You can find great investment properties at tax sales. What is a tax sale? How does a tax sale work? Keep reading for an introduction to the basics of tax sales.

County collectors are required to collect delinquent property taxes. In addition to county taxes, county collectors may also collect delinquent taxes for cities and towns, but some cities conduct their own tax sales to collect delinquent taxes. The Collector is the only public official given the responsibility for collecting delinquent taxes for the county. The statutory method for collecting delinquent real estate taxes is through the tax sale. The Collector is usually required to collect the entire amount of taxes, penalties, and interest due on the property. Collectors apply tax payments first to the payment of back taxes and then to payment of current taxes. Payment is applied to the oldest delinquent taxes first.

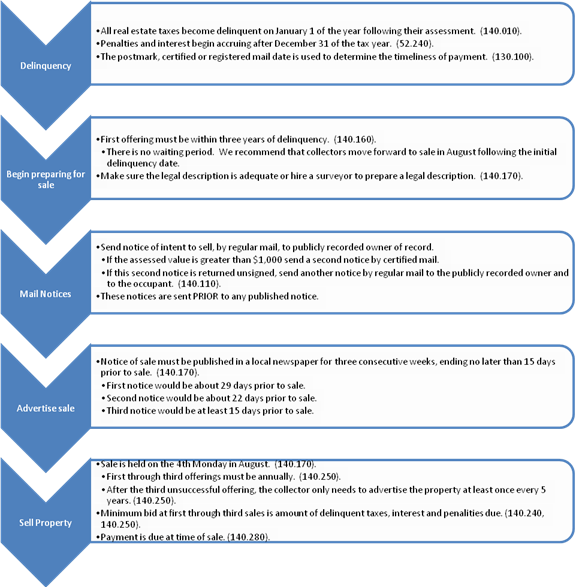

All real estate taxes become delinquent on January 1 of the year following their assessment. Penalties and interest begin accruing after December 31 of the tax year. Each year the collector sends out a statement showing the taxes due. That statement includes a statement of delinquent taxes, penalties, and interest due. The county collector is required to make a list of delinquent taxes. This list is then submitted to the county commission for review and correction. After the commission review, the county clerk prepares the back tax book.

Each year, the county has a tax sale. Prior to the sale, the collector must send notice to the publicly recorded owner of record. Additionally, the collector must publish a list of delinquent lands and lots in a newspaper of general circulation within the county. Lists must be published once a week for three consecutive weeks prior to the sale. Delinquent tax sales begin at 10:00 a.m. on the fourth Monday in August and run from day to day until all parcels are offered for sale. At the first three offerings, properties must be sold for a sufficient amount as to pay the taxes, interests, and charges owed on the property or chargeable to the taxpayer in that county. Individuals who are delinquent on any tax payments, other than a delinquency on the property being offered, cannot purchase property at a tax sale. Individuals who are not Missouri residents must appoint a county citizen to act as their agent and for service of process. A purchaser at tax sale is required to immediately pay his bid to the collector. In addition to the right of redemption, the publicly recorded owner has three years to collect any surplus funds from the tax sale, which are held in the county treasury.

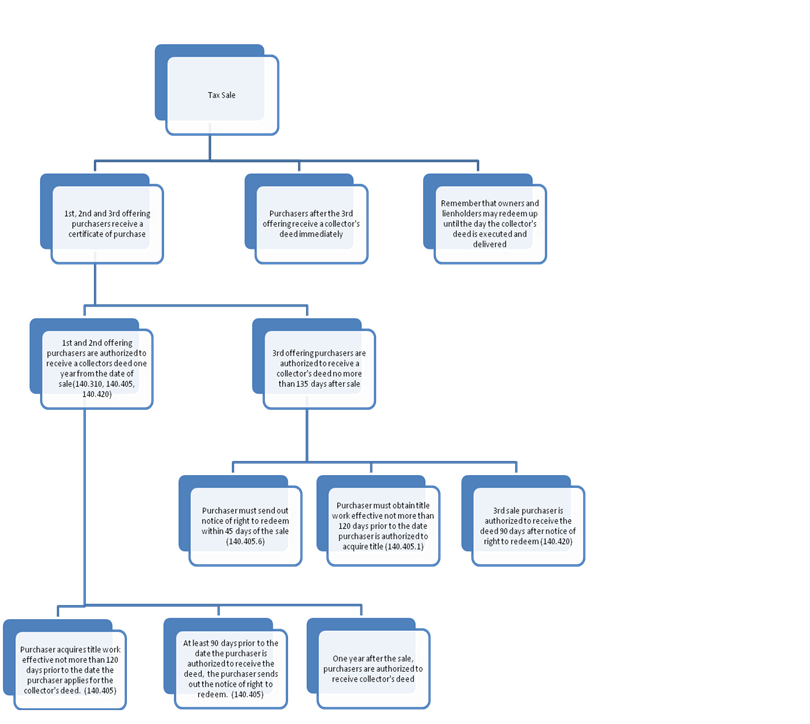

After a purchaser pays his or her bid, the county collector issues a written certificate of purchase. The certificate of purchase creates a lien on the property. The Collector’s Deed acts to transfer title to the property. Before a purchaser can request that a deed be issued, and at least ninety days prior to the date when a purchaser is authorized to acquire the deed, the purchaser must notify interested parties of the right to redeem. The owner has a superior interest to the purchaser and can redeem prior to the sale, or up until the Collector’s Deed is issued to the purchaser. However, the person redeeming the property must pay the costs incurred by the purchaser. Purchasers must provide an affidavit that every notice requirement has been met. The purchaser is entitled to a Collector’s Deed when:

After a purchaser pays his or her bid, the county collector issues a written certificate of purchase. The certificate of purchase creates a lien on the property. The Collector’s Deed acts to transfer title to the property. Before a purchaser can request that a deed be issued, and at least ninety days prior to the date when a purchaser is authorized to acquire the deed, the purchaser must notify interested parties of the right to redeem. The owner has a superior interest to the purchaser and can redeem prior to the sale, or up until the Collector’s Deed is issued to the purchaser. However, the person redeeming the property must pay the costs incurred by the purchaser. Purchasers must provide an affidavit that every notice requirement has been met. The purchaser is entitled to a Collector’s Deed when:

(1) the ninety day right to redeem notice has been met;

(2) the affidavit concerning notice requirements has been filed; and

(3) the one year redemption period has expired.

If no person redeems the property within one year from the sale date of a first or second offering sale or within the 90 day redemption period for a third offering sale, upon the production of a certificate of purchase, the collector shall execute a deed to the purchaser which shall vest the grantee with an absolute estate in fee simple. However, failure to comply with notice requirements results in the purchaser’s loss of all interest in the real estate.

Many purchasers take the additional step of obtaining a judgment quieting the title to the property (often required by a title company as a condition of issuing a title insurance policy). The attorneys at the Paul Law Firm regularly pursue quiet title actions for our clients who have purchased properties at tax sales in McDonald, Newton, and Jasper counties in particular. Please note that tax sales are extremely technical, and this article is intended as an introductory overview.

Many purchasers take the additional step of obtaining a judgment quieting the title to the property (often required by a title company as a condition of issuing a title insurance policy). The attorneys at the Paul Law Firm regularly pursue quiet title actions for our clients who have purchased properties at tax sales in McDonald, Newton, and Jasper counties in particular. Please note that tax sales are extremely technical, and this article is intended as an introductory overview.

If you have additional questions about tax sales, call or come visit the attorneys at the Paul Law Firm. Consultations are always free!

Check out the Missouri State Tax Commission’s “Tax Sale Procedure Manual.”